Understanding How Bank Payments Actually Work

Understanding How Bank Payments Actually Work

SWIFT, NPP, Clearing, Settlement and the Hidden Architecture of Modern Banking

Most people think sending money through a banking app is simple.

You open your banking app, enter the amount, press Send, and within seconds the money appears in the recipient’s account.

But behind that simple action lies an extremely complex network of financial systems, payment rails, settlement services, and security layers.

In this post, we will go through:

The difference between SWIFT and NPP

How modern payment systems work

The meaning of clearing, settlement, and reconciliation

The hidden architecture inside banks

How engineers debug a failed payment

Let’s start from the beginning.

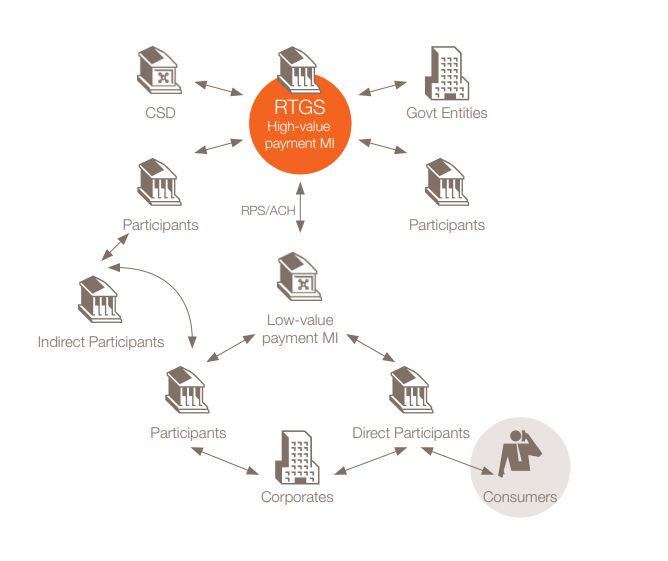

1. The Different Payment Rails Banks Use

Banks don’t use a single payment system. They use multiple payment rails, each designed for different purposes.

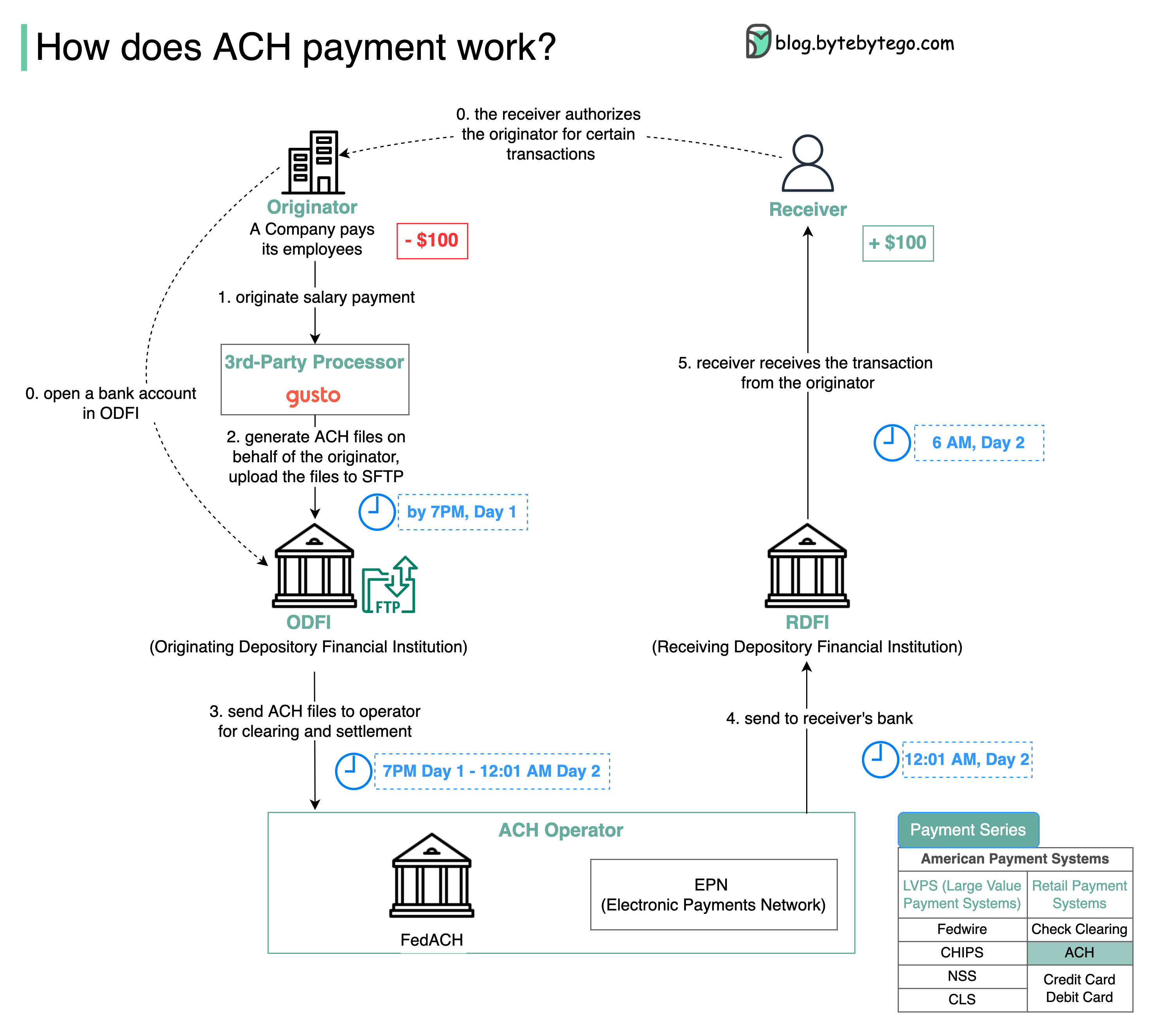

ACH – Batch Payments

ACH-style systems process payments in batches.

These are commonly used for:

Salary payments

Utility bills

Direct debit

Subscription payments

Instead of processing transactions instantly, banks collect transactions and process them together at scheduled times.

This is efficient for high-volume payments, but it is not instant.

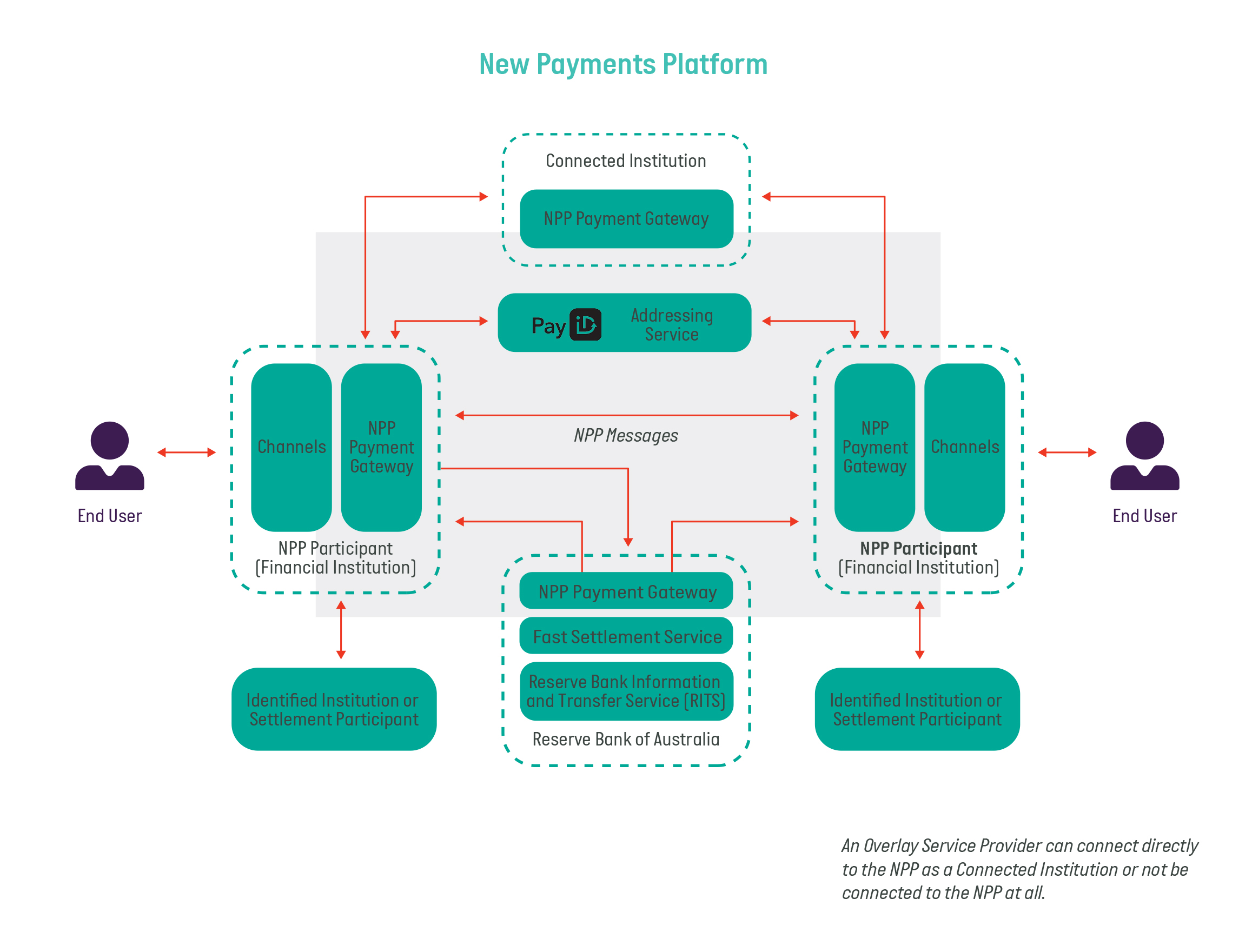

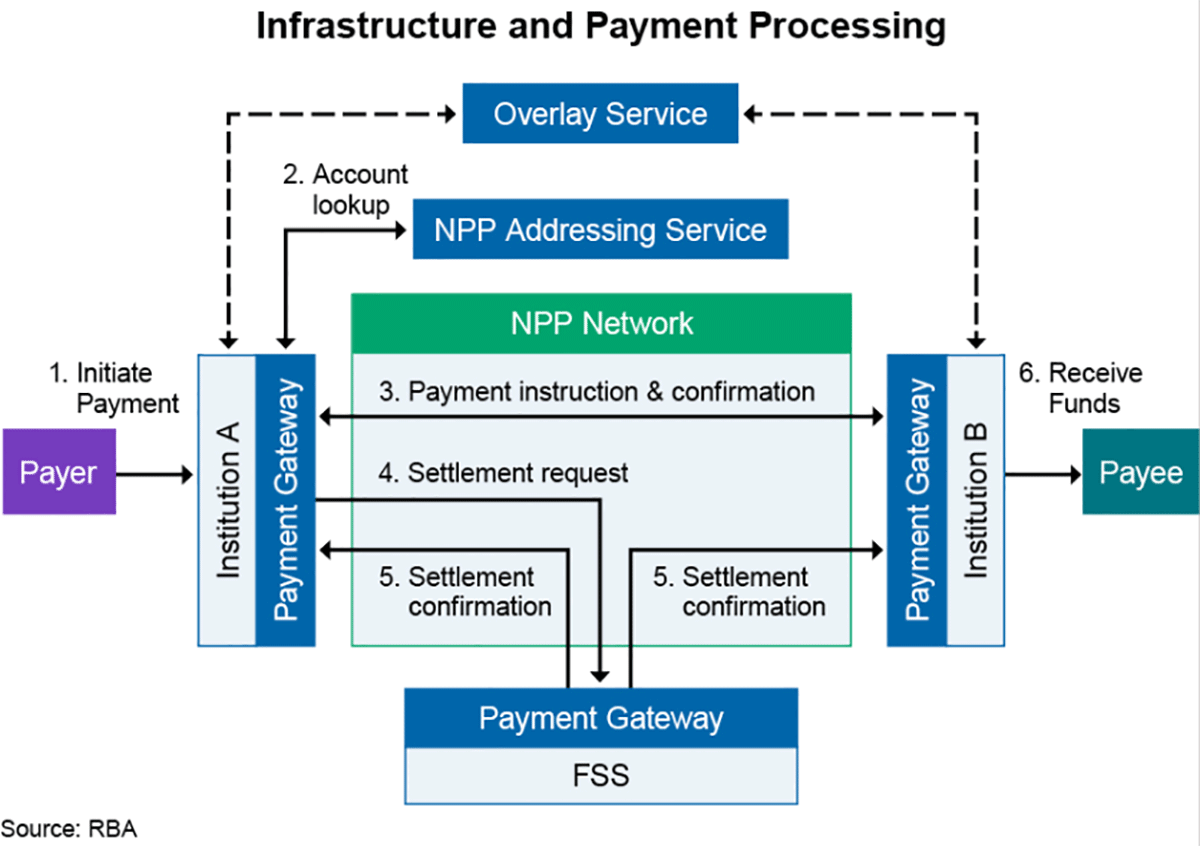

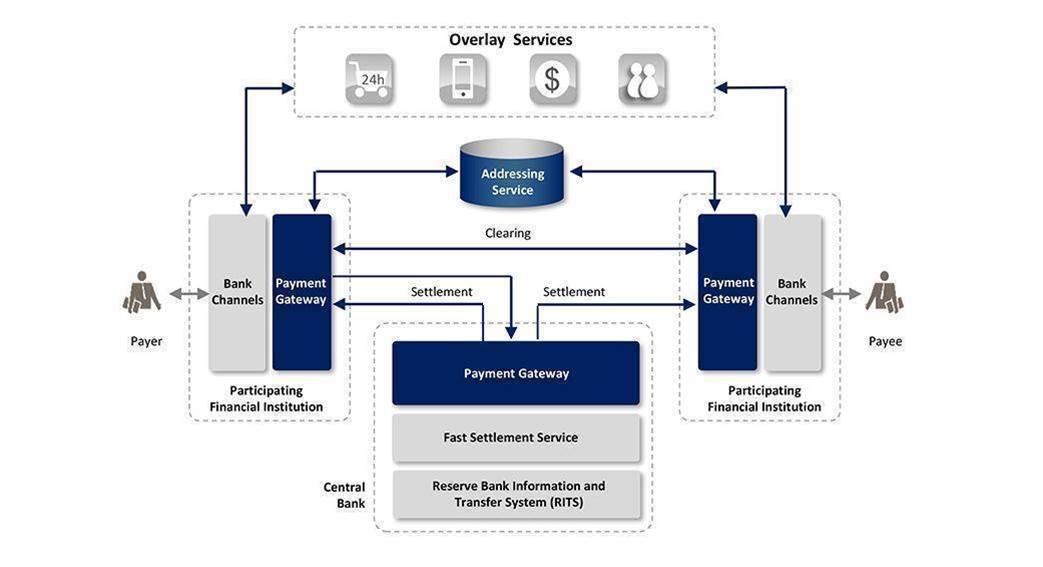

NPP – Instant Payments (Australia)

Australia introduced the New Payments Platform (NPP) to enable real-time payments.

With NPP:

Payments happen within seconds

The system works 24/7

Transfers can use PayID (phone number or email)

Settlement occurs through systems operated by the

Reserve Bank of Australia.

This is why when you transfer money between banks today, it often arrives almost instantly.

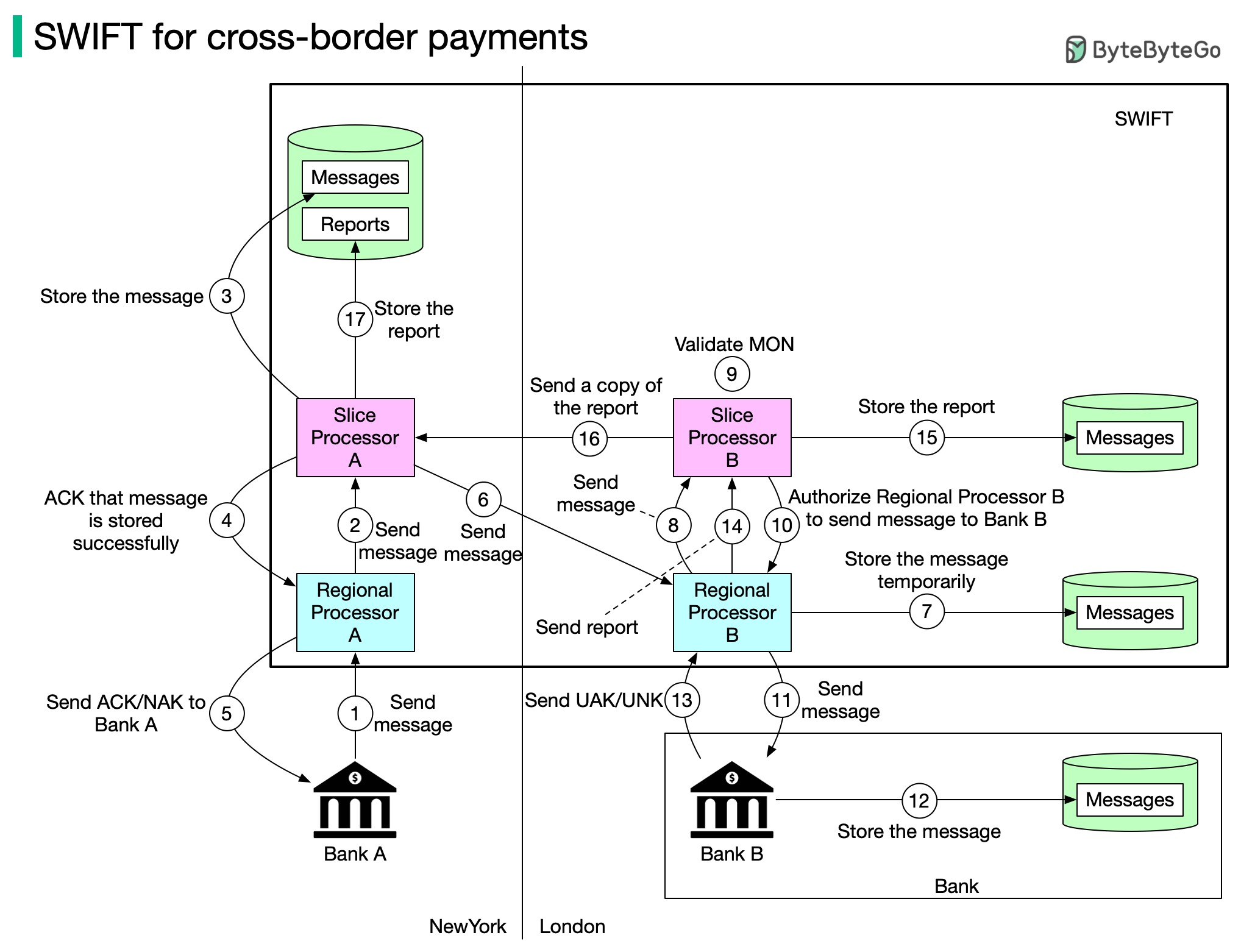

SWIFT – International Payments

When money moves between countries, banks rely on the global network known as

SWIFT is not a payment system.

Instead, it is a secure messaging network used by banks to send payment instructions.

The actual movement of money happens later through correspondent banking relationships.

This is why international transfers can take 1–3 days.

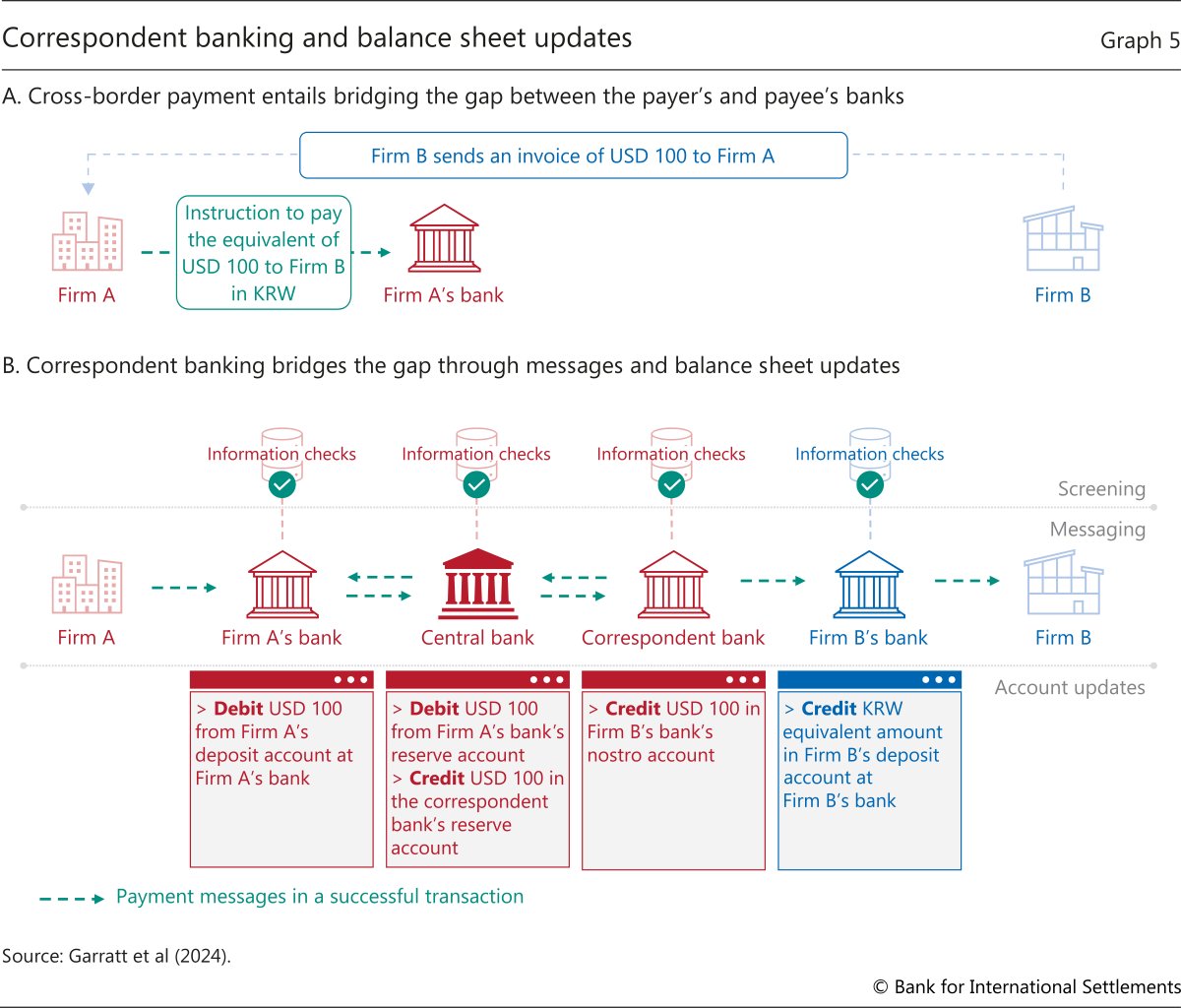

2. The Three Stages of Every Payment

Every banking payment goes through three important stages.

Clearing

Clearing is when banks exchange payment instructions.

At this stage:

Payment messages are verified

The receiving bank confirms account details

The system calculates who owes money to whom

Important:

No money moves yet.

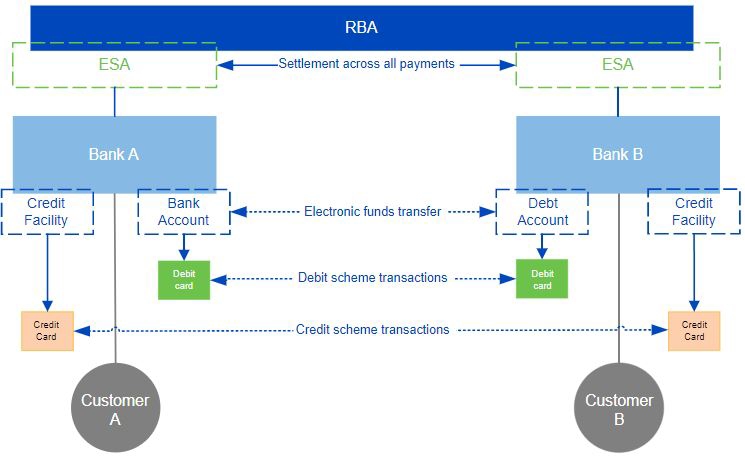

Settlement

Settlement is when the actual money moves between banks.

This usually happens through accounts held at the central bank.

Once settlement occurs:

The payment becomes final

It cannot easily be reversed

Reconciliation

Reconciliation ensures that all financial records match.

Banks compare:

Payment network logs

Core banking records

Settlement records

Transaction ledgers

If something doesn't match, it triggers a manual investigation.

3. What Happens When You Send Money

Here is the simplified journey of a payment.

Mobile Banking App

↓

API Gateway

↓

Fraud Detection

↓

Payment Processing System

↓

Clearing Network

↓

Central Bank Settlement

↓

Recipient Bank

↓

Recipient Account Credited

In modern real-time systems like NPP, this entire process happens in just a few seconds.

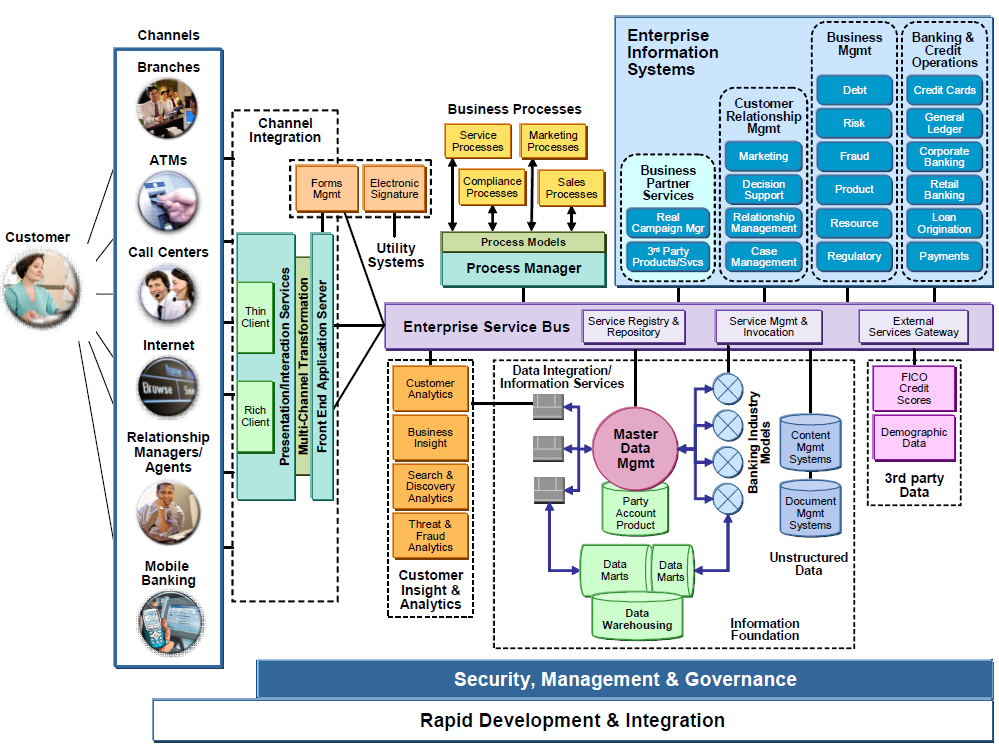

4. The Hidden Architecture Inside Banks

Modern banks are built from several major systems.

Typical architecture includes:

Customer Channels

Mobile apps

Internet banking

ATMs

API Gateway

Routes requests

Enforces security

Fraud & Risk Systems

Detect suspicious transactions

Apply security policies

Payment Processing Systems

NPP

Card networks

SWIFT

The bank’s main ledger

Stores account balances

Data & Analytics Systems

Reporting

Compliance

Fraud monitoring

5. How Banks Debug a Failed Payment

Payments pass through many distributed systems, which means failures can happen at different points.

Engineers investigate using:

Transaction IDs

Every payment has a unique identifier.

Example:

TXN-8934729384

This ID appears in logs across multiple systems.

Observability Tools

Banks monitor payments using:

Logs – detailed system events

Metrics – performance data

Traces – end-to-end request tracking

These tools help engineers trace exactly where a payment failed.

Example Failure

Transaction ID: TXN-8934729384

Mobile App → OK

API Gateway → OK

Fraud Engine → OK

Payment Processor → OK

Settlement System → FAILED

Reason: Liquidity issue

Once engineers identify the failure point, they can investigate and resolve the issue.

Final Thoughts

Banking systems may appear simple from the outside, but internally they are one of the most complex distributed systems in the world.

Every time you send money:

Multiple systems validate the transaction

Payment networks exchange instructions

Central banks settle the funds

Banks reconcile records across multiple ledgers

And all of this often happens within seconds.

Understanding this architecture is not only fascinating — it is also essential knowledge for anyone working in fintech, payments, or financial technology engineering.

Comments

Post a Comment